In the fast-paced world of finance, businesses often find themselves juggling various financial challenges. One such challenge is managing accounts receivable, a vital aspect of cash flow. To address this issue, a financial solution known as factoring has emerged as a game-changer for businesses of all sizes.

What is Factoring in Accounts Receivable?

Factoring, in the context of accounts receivable, is a financial practice where a business sells its unpaid invoices (accounts receivable) to a third-party financial institution or a specialized company called a factor. In return, the business receives an immediate cash advance, typically a percentage of the total invoice value, which allows for improved cash flow. The factor, in turn, assumes the responsibility of collecting payments from the customers.

Factoring is an attractive financial tool for businesses that face cash flow constraints due to slow-paying customers or need quick access to funds for various operational needs. It’s important to note that factoring is not a loan; it’s the sale of an asset (accounts receivable) at a discount to secure immediate funds.

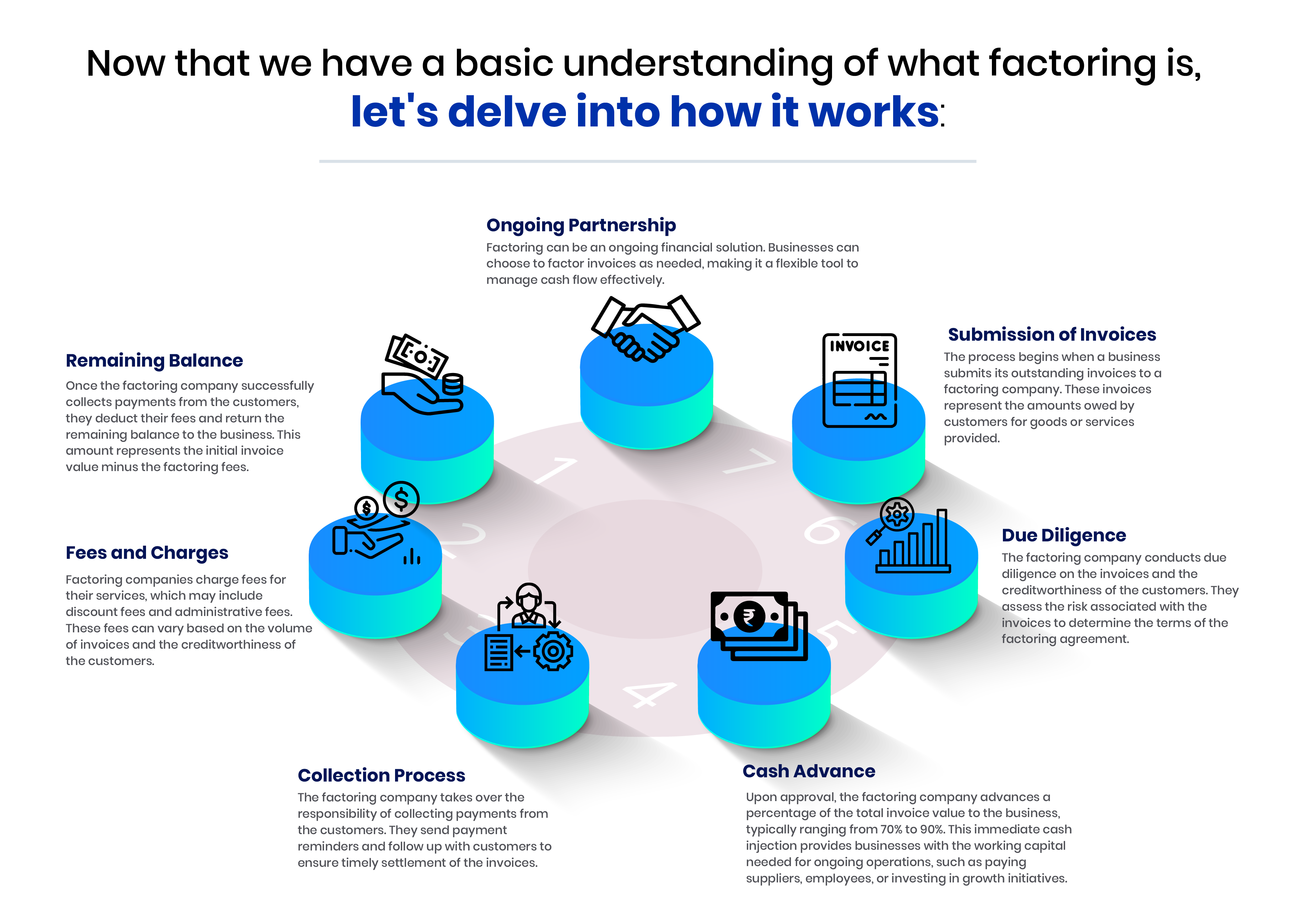

How Factoring Accounts Receivable Works

In conclusion, factoring accounts receivable offers a practical way for businesses to improve cash flow and maintain financial stability. By outsourcing the collection of unpaid invoices to specialized factoring companies, businesses can focus on their core operations and growth while ensuring a steady influx of working capital. Factoring is a valuable financial strategy that empowers businesses to thrive in today’s competitive markets.

Types of Factoring in Accounts Receivable

Factoring in accounts receivable comes in various forms to cater to the specific needs of different businesses. Here are the common types of factoring:

- Recourse Factoring:

In this type, the business remains responsible for any unpaid invoices if the customer fails to make payment within the agreed-upon time frame.

It’s a riskier form of factoring for the business, but it often comes with lower fees.

- Non-Recourse Factoring:

With non-recourse factoring, the factoring company assumes the full credit risk for the invoices. If a customer doesn’t pay, the business isn’t held accountable.

However, non-recourse factoring usually involves higher fees due to the decreased risk to the business.

- Spot Factoring:

Spot factoring allows businesses to selectively factor individual invoices rather than their entire accounts receivable portfolio.

This flexibility is ideal for companies that don’t want to commit to long-term factoring agreements.

- Invoice Discounting:

Invoice discounting is a confidential form of factoring where the business retains control over collecting payments from its customers.

The factoring company provides an advance based on the invoices but doesn’t interfere with customer relationships.

- Bulk or Whole Turnover Factoring:

In this comprehensive form of factoring, a business factors all of its invoices, providing consistent cash flow but relinquishing control over the collection process.

- Export Factoring:

Export-focused businesses can use export factoring to manage international invoices. The factoring company handles the complexities of cross-border transactions and currency conversions.

Each type of factoring offers its own advantages and considerations, making it crucial for businesses to choose the one that aligns with their financial goals and risk tolerance.

How is This Different from Accounts Financing

While factoring and accounts financing may seem similar, they are distinct financial solutions:

Factoring:

- Factoring involves selling accounts receivable (unpaid invoices) to a third party (the factor) at a discount in exchange for immediate cash.

- It is essentially a sale of assets, not a loan, so it doesn’t create debt on the balance sheet.

- The factor assumes the responsibility for collecting payments from customers.

Accounts Financing (Accounts Receivable Financing):

- Accounts financing, also known as accounts receivable financing or invoice financing, is a loan-based approach.

- Instead of selling invoices, a business uses its accounts receivable as collateral to secure a loan from a financial institution.

- The business retains ownership of the invoices and is responsible for collecting payments from customers.

- Accounts financing involves paying interest on the loan, which can be more cost-effective for businesses with a strong credit history.

In summary, factoring focuses on selling invoices to obtain immediate cash flow, while accounts financing involves using accounts receivable as collateral to secure a loan. The choice between these two financial strategies depends on a business’s specific needs, risk tolerance, and financial objectives. Both options offer ways to leverage accounts receivable for improved liquidity and working capital.

Eligibility for Factoring Accounts Receivables

Not all businesses are automatically eligible for factoring accounts receivables. Factoring companies have certain criteria that businesses must meet to qualify for their services. Here are some common eligibility factors:

Creditworthiness of Customers: Factoring companies assess the creditworthiness of your customers since they will be responsible for collecting payments. Customers with a history of late payments or financial instability may affect your eligibility.

Invoice Quality: The invoices you want to factor should be clear and accurate, with no disputes or legal issues surrounding them.

Business Type: Factoring is available to a wide range of businesses, but some industries may face more challenges in securing factoring services due to their specific characteristics or regulatory requirements.

Invoice Volume: Factoring companies often have minimum and maximum invoice volume requirements. Your business should generate a sufficient number of invoices to make factoring cost-effective.

Financial Health: Some factoring companies may assess your business’s financial stability and creditworthiness as part of the eligibility process.

Contractual Agreements: Any existing agreements or contracts that prohibit the sale of invoices (recourse) may impact your eligibility for non-recourse factoring.

It’s essential to discuss your specific business situation with potential factoring partners to determine your eligibility and find the best fit for your needs.

Choosing the Right Accounts Receivable Factoring Partner

Selecting the right accounts receivable factoring partner is a critical decision that can significantly impact your business’s financial health. Here are some key factors to consider when choosing a factoring company:

Experience and Reputation: Look for a factoring company with a solid track record and a reputation for reliability and transparency. Check online reviews and ask for references.

Specialization: Some factoring companies specialize in certain industries or invoice types. Choose one that understands your business and its unique needs.

Terms and Fees: Compare the terms and fees offered by different factoring companies. Pay close attention to discount rates, processing fees, and any hidden charges.

Customer Service: A responsive and supportive customer service team is invaluable. You’ll want a partner that is readily available to address your questions and concerns.

Collection Practices: Understand the factoring company’s collection methods and how they interact with your customers. Clear communication is essential to maintain positive customer relationships.

Flexibility: Ensure that the factoring company’s terms align with your business’s growth plans and financial goals. Some factors offer flexible contracts that can adapt to your changing needs.

Transparency: Transparency in the factoring process is crucial. You should have access to detailed reports on the status of your invoices and collections.

Contractual Terms: Carefully review the factoring agreement, including any recourse or non-recourse clauses, termination policies, and notice periods.

Choosing the right accounts receivable factoring partner can be a transformative decision for your business, providing access to the working capital needed for growth and stability.

Conclusion

In conclusion, factoring accounts receivables is a powerful financial tool that can help businesses overcome cash flow challenges and unlock growth opportunities. However, eligibility for factoring depends on various factors, including customer creditworthiness, invoice quality, and your business’s financial health.

Remember, factoring accounts receivables can be a valuable tool for businesses of all sizes and industries. Whether you’re a small startup looking to bridge cash flow gaps or an established company seeking to fuel expansion, factoring can provide the financial stability you need to thrive.

Don’t let cash flow constraints hold your business back. Take the next step towards financial empowerment by exploring the possibilities of factoring accounts receivables today. Your business’s success and growth may depend on it.